Support CleanTechnica’s work through a Substack subscription or on Stripe.

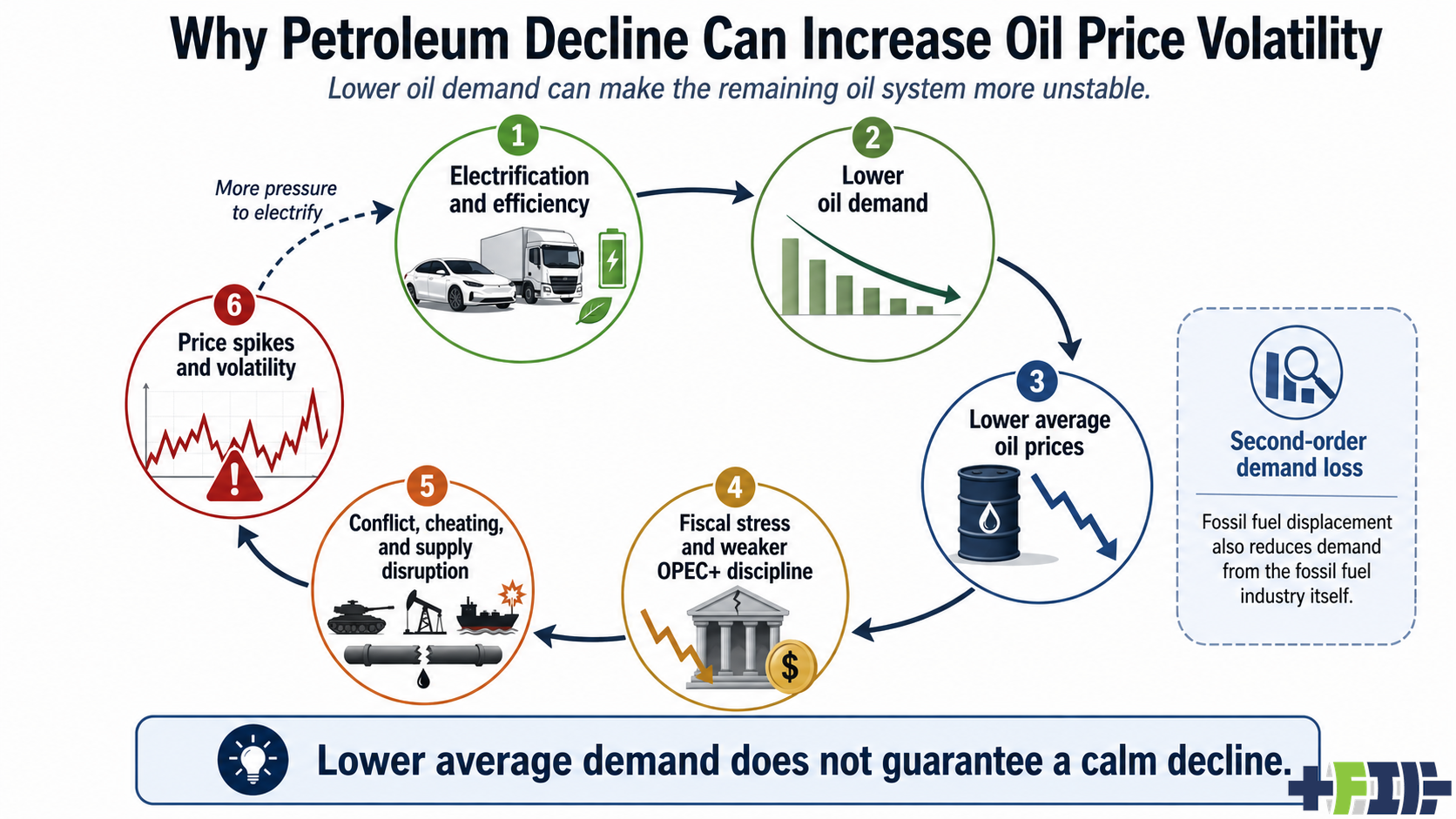

The UAE’s decision to leave OPEC+ is not just another Gulf oil story. It is an early signal of what happens when a producer with low-cost barrels, spare capacity ambitions, and a long view of electrification decides that flexibility may be worth more than cartel discipline. Oil demand is beginning to bend under the weight of EVs, electric trucks, efficiency, remote work, substitution, and changing logistics. That should suggest a calmer oil market, with lower prices as the world uses less petroleum. But the more interesting possibility is the opposite. The petroleum system is more likely to become less stable as it declines, because the institutions, companies, states, supply chains, and fiscal bargains built around oil were built for growth. A declining oil market does not just reduce demand. It changes incentives.

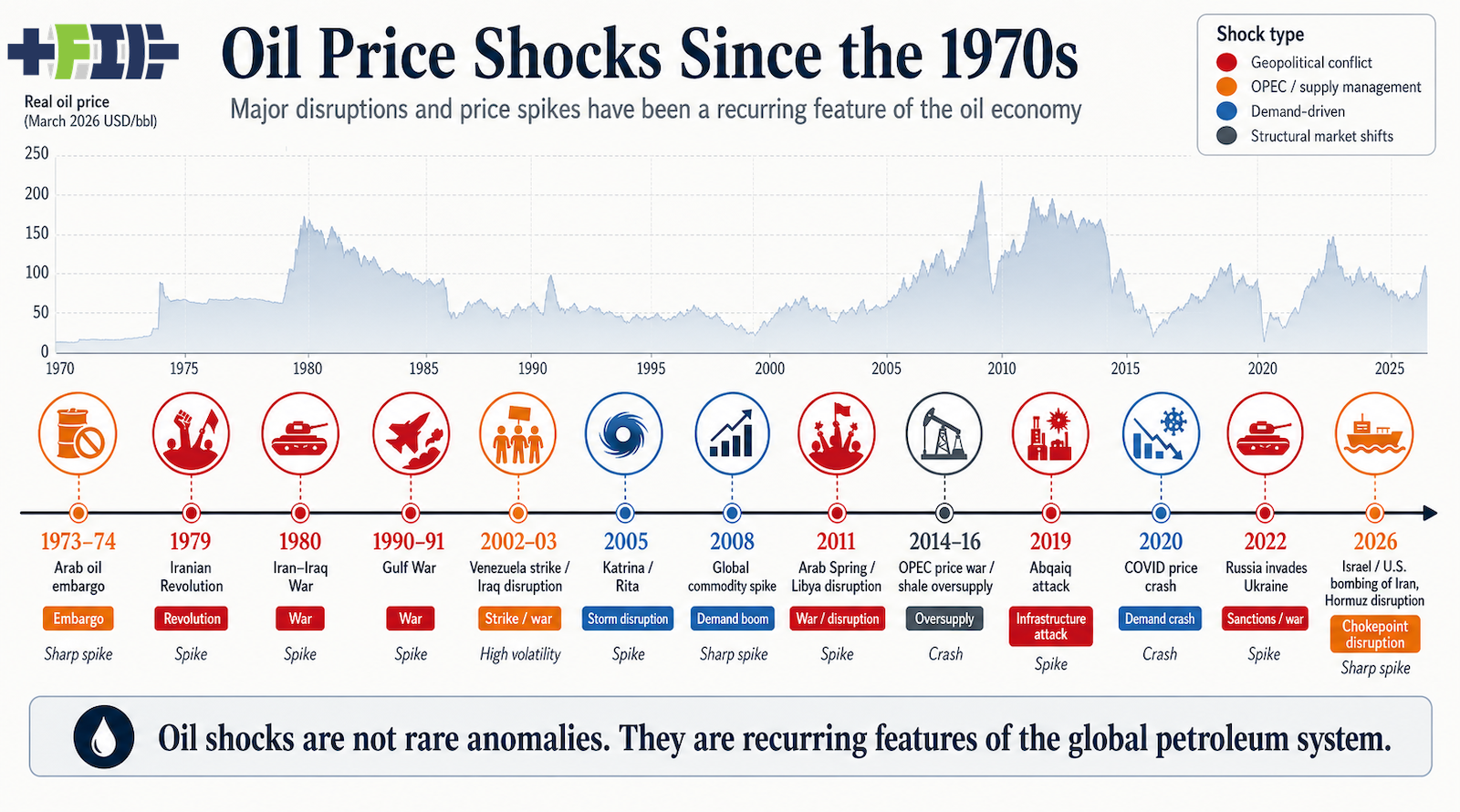

Oil shocks have too often been treated as interruptions to the normal petroleum economy. The better way to understand them is as recurring features of that economy. Since the early 1970s, the world has had the Arab oil embargo, the Iranian Revolution, the Iran-Iraq War, the first Gulf War, the Venezuela strike and Iraq disruption, Hurricane Katrina and Hurricane Rita, the 2008 commodity spike, the Arab Spring and Libyan disruption, the 2014 to 2016 OPEC price war, the 2019 Abqaiq attack, the 2020 COVID price crash, Russia’s 2022 invasion of Ukraine, and now the 2026 Iran and Hormuz crisis. Some were supply shocks. Some were demand shocks. Some were wars, cartel-management failures, weather events, infrastructure failures, and crashes rather than spikes. The common feature is that the petroleum system has produced instability again and again.

{kind=link}

The 1973 to 1974 Arab oil embargo is still the defining image of modern oil vulnerability. Federal Reserve historical material notes that the embargo helped push oil from roughly $2.90/bbl before the embargo to $11.65/bbl by January 1974. That was not just a price movement. It was a political and economic signal that oil was not an ordinary commodity. It was tied to foreign policy, military logistics, inflation, trade balances, consumer confidence, and the physical movement of goods and people. Once the world learned that lesson, it kept relearning it.

The next shocks showed that petroleum instability could come from almost anywhere in the system. The 1979 Iranian Revolution and the 1980 Iran-Iraq War showed that oil markets are vulnerable not only to producer policy, but to the internal stability of producer states and the security of the regions around them. The 1990 to 1991 Gulf War was a chokepoint and regional-security shock. The early 2000s brought Venezuela’s strike and the Iraq war period. Katrina and Rita showed that a wealthy importing and producing country could still suffer product-market stress from refinery, port, and pipeline disruption.

The modern period added new forms of volatility. The 2008 spike showed how demand growth, financial pressure, and constrained supply can produce a price surge without a single neat military trigger. The 2011 Libya disruption showed how political upheaval in one producer can matter when the market is tight. The 2014 to 2016 price collapse showed that OPEC strategy and shale growth could produce a different kind of shock, one that damaged producer revenues rather than consumer budgets. The 2020 COVID crash showed that demand destruction can be violent enough to push parts of the oil market into absurd territory, including negative WTI futures in April 2020. The 2022 Russia shock reminded the world that oil and gas are embedded in war, sanctions, shipping, insurance, and finance.

The current Strait of Hormuz shock is not a replay of the 1973 to 1974 OPEC embargo, but it rhymes with it in important ways. The 1970s shock was a producer-country political embargo that showed importing economies how exposed they were to concentrated oil supply. The 2026 shock is a physical chokepoint and infrastructure crisis layered onto war, shipping risk, LNG disruption, aviation rerouting, insurance costs, and already-weakened oil demand. Fatih Birol of the International Energy Agency has described it in far stronger terms than the usual oil-market language, calling the current crisis “the biggest crisis in history” and saying it is more serious than the 1973, 1979, and 2022 crises combined. The IEA’s April 2026 Oil Market Report called it “the most severe oil supply shock in history,” noting that oil prices posted their largest-ever monthly gain in March and that North Sea Dated crude was trading around $130/bbl, about $60/bbl above pre-conflict levels. The IEA has also said the volume of fuel supply offline is higher than during the 1973 shock that led to the agency’s creation, with Hormuz normally carrying around 20 million barrels per day of crude oil and oil products, about one-fifth of global oil consumption. The comparison matters because the 1970s shock created the modern energy-security system. This one is exposing how much of that system still rests on oil moving through narrow sea lanes, fragile regional politics, and producer states whose incentives are changing as electrification erodes the old demand-growth bargain.

The inflation-adjusted monthly oil price chart in the infographic above makes this visible. In nominal terms, the 1970s look small because dollars have changed so much. In March 2026 dollars, the 1970s and early 1980s shocks become large again, and the 2008 and 2011 to 2014 period stand out as a prolonged high-price era. The point is not that every shock is identical. The point is that oil has never been a smooth input into the global economy.

The old oil-stability model worked as well as it did because demand was expected to grow. OPEC and later OPEC+ could ask members to restrain supply today because the unsold barrel was expected to be valuable tomorrow. That is the central bargain of a producer cartel in a growing market. If everyone believes future demand will be larger, then discipline today can raise total revenue over time.

That bargain was always imperfect. OPEC has always had quota cheating, baseline fights, Saudi frustration, producer rivalries, and non-OPEC supply responses. High prices encouraged conservation, efficiency, offshore exploration, unconventional oil, and eventually shale. Low prices stressed public budgets and led to overproduction. Saudi Arabia acted as swing producer when it thought the bargain was worth maintaining, but it has also chosen market-share fights when the burden became too uneven. OPEC cohesion has never been a permanent fact. It has been a repeated negotiation.

OPEC+ was a recognition that OPEC alone no longer controlled enough of the global oil system. The addition of Russia and other producers gave the group more scale, but it also made coordination harder. Russia’s incentives are not Saudi Arabia’s incentives. Kazakhstan’s incentives are not Iraq’s. The UAE’s incentives are not Algeria’s. In a growing market, those differences can be managed. In a shrinking market, they become harder to paper over.

Electrification changes the psychology of the barrel. The old bargain was simple: restrain supply today because the unsold barrel should be valuable tomorrow. Electrification weakens that bargain by making the deferred barrel look less like stored value and more like future risk. That is a profound change in producer incentives. It does not require oil demand to crash overnight. It only requires enough producers to believe that demand growth is ending and that the long-term curve is no longer their friend.

This is where the UAE’s exit from OPEC matters. It is not just a quota dispute. It is a signal from a wealthy, capable, low-cost Gulf producer that flexibility and volume may be worth more than cartel discipline. The UAE has invested heavily in production capacity. If it can sell more barrels outside the quota structure, it has a rational reason to do so, especially if it believes future demand is uncertain. Other producers will notice.

The demand side is moving faster than oil institutions were designed to handle. Passenger EVs are now mainstream in China and Europe and are moving into many other markets. Electric buses are normal in China and common in many cities. Electric two-wheelers and three-wheelers have already displaced petroleum demand across parts of Asia. Delivery fleets are electrifying because depot charging, predictable routes, and high use rates make the economics work. The new pressure point is heavy trucking, where China is already showing that battery-electric trucks can move from niche to material market share. When a segment as diesel-heavy as trucking starts to bend, oil demand forecasts have to change.

China matters because it was the central oil-demand growth story for a generation. If Chinese gasoline and diesel demand are flat or declining while GDP continues to grow, the relationship between economic growth and oil demand is breaking. That is not a small adjustment. It is a signal that electrification, rail, logistics efficiency, and industrial policy are changing the demand structure. The International Energy Agency has already noted that Chinese gasoline and diesel demand have stopped behaving like the old middle-income growth story. IEEFA has reported that battery-electric heavy-duty trucks reached close to 22% of Chinese heavy-duty vehicle sales in the first half of 2025, up from under 9% a year before. That is a large change in a segment that many oil forecasts treated as resistant to electrification.

Aviation is often used as the refuge of oil demand. Passenger cars electrify, buses electrify, some trucks electrify, but jets still burn liquid fuel. That is true physically, but it does not mean aviation demand is a growth savior. COVID normalized remote work and video meetings. Business travel did not recover as if nothing had happened. The 2026 Gulf disruption has again made aviation through the region more expensive and less reliable. The EU is pricing aviation emissions and requiring sustainable aviation fuel blending. Jet fuel can remain hard to replace while aviation demand is flat or pressured. Those two facts can coexist.

A flat aviation sector is a problem for bullish oil demand models. If road fuels decline and aviation only holds steady, aviation does not offset the loss. If jet fuel prices spike because of war risk, rerouting, insurance, or fuel supply problems, some trips disappear, some meetings move back to Zoom, and some companies rediscover that the cheapest barrel is the one they do not buy. Aviation is not immune to price and risk. It is just harder to electrify directly.

There is another demand effect that is easy to miss. The fossil fuel industry is one of the world’s largest consumers of fossil fuels. Exploration, drilling, pumping, steam generation, upgrading, refining, liquefaction, compression, pipeline operations, shipping, mining, and petrochemical processing all require energy. Much of that energy is fossil. When a ton of fossil fuel demand disappears from the end-use economy, some fraction of the energy used to produce, process, and deliver that ton also disappears. The effect varies by fuel, region, and production pathway, but the direction is clear. A refinery running less hard uses less energy. A shale basin drilling fewer wells uses less diesel, less sand hauling, less water handling, and less steel movement. A smaller LNG buildout means fewer compressors, ships, and terminals. A smaller petroleum system has a smaller petroleum support system.

The feedback loop is straightforward. Electrification and efficiency reduce oil demand. Lower oil demand weakens average prices and growth expectations. Lower prices increase fiscal stress in producer states. Fiscal stress weakens subsidies, public payrolls, patronage networks, security arrangements, debt service, imports, and regional bargains. That raises the risk of internal instability, quota cheating, sabotage, coups, strikes, sanctions escalation, export interruptions, and regional conflict. Those events cause oil-price spikes. The spikes increase the pressure to electrify and hedge against oil. That reduces future demand. The loop repeats.

High oil prices make electrification economically attractive. Volatile oil prices make electrification institutionally attractive. A fleet operator does not only care about today’s diesel price. It cares about whether diesel can blow up its budget next year. A city transit agency does not only care whether electric buses save money at average fuel prices. It cares whether a geopolitical shock can force an emergency budget request. A delivery company does not only compare the spot price of diesel with the cost of electricity. It compares exposure to OPEC+, Hormuz, sanctions, refineries, and currency swings with a depot charging strategy that can include long-term power contracts, on-site solar, batteries, and managed charging.

Lower average demand does not guarantee a calm decline. It can produce lower average prices, more fragile producers, and more frequent shocks. In a growing market, a price shock is often followed by new investment because the long-term demand story remains intact. In a declining market, investors become more cautious. They do not want to fund long-cycle oil projects that may arrive into a weaker market. But existing fields decline. Demand does not fall evenly by product, region, or season. The result can be periods of oversupply followed by sudden tightness.

That is how oil can lose long-term pricing power while gaining short-term volatility. Producers pump through low prices because they need cash. OPEC+ discipline weakens because every member wants revenue. Investment falls because capital sees peak demand risk. A fragile producer then loses output, a port closes, a pipeline is attacked, sanctions tighten, or a chokepoint becomes unsafe. Prices spike. The spike accelerates substitution. Demand falls again. Producers become more fiscally stressed. The next shock becomes more likely.

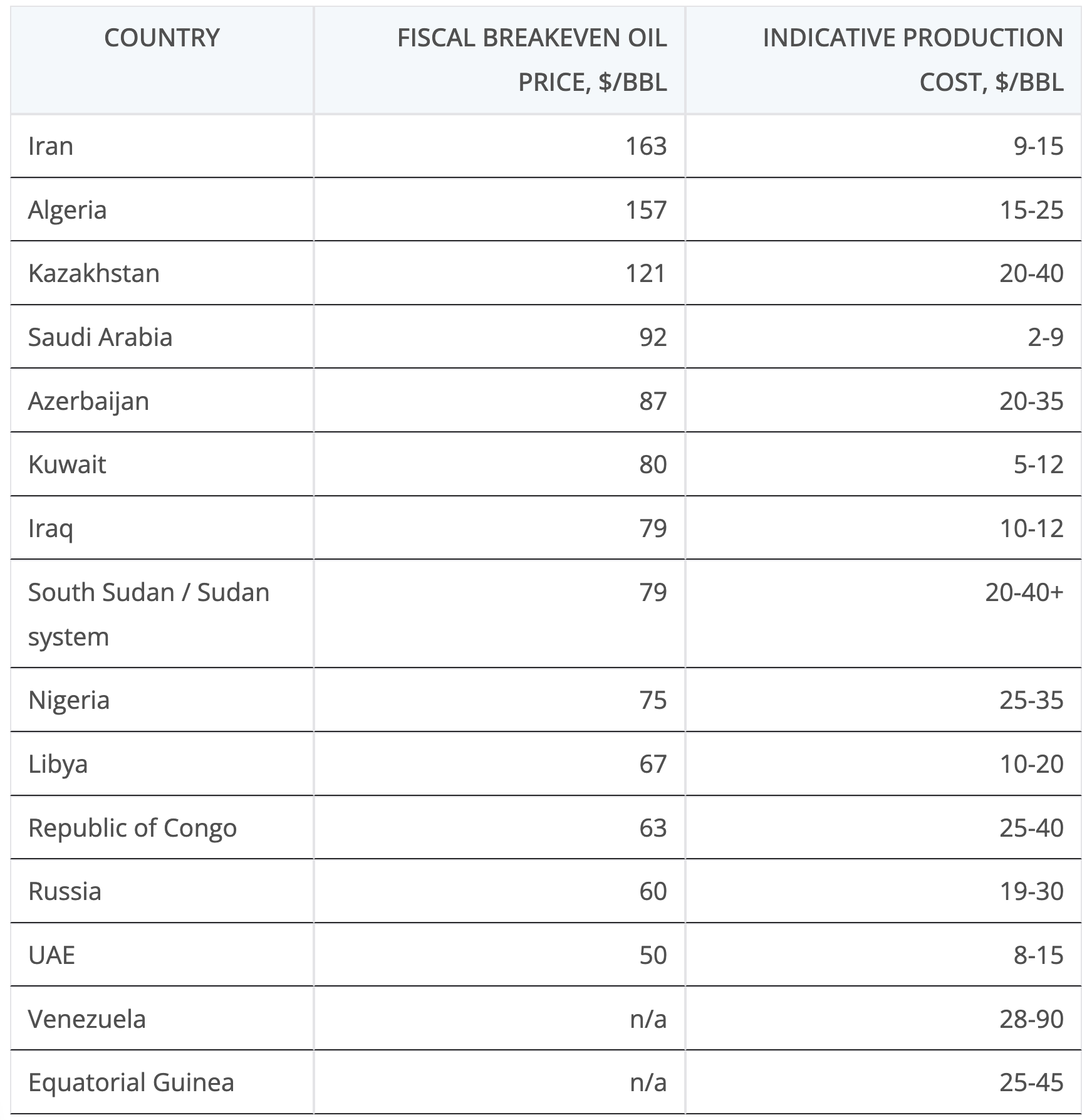

The distinction between production cost and fiscal stress is central. Many OPEC barrels are cheap. Saudi, Kuwaiti, Iraqi, Emirati, and Iranian barrels are not generally the expensive barrels that disappear first. In pure lifting-cost terms, much of the Gulf and parts of the Middle East remain among the most resilient oil regions in the world. If the question is which barrels survive a lower-price world, the answer is often the low-cost Middle Eastern barrels.

But production cost is not the same thing as political resilience. Fiscal breakeven is not the cost of producing oil. It is the oil price needed to fund the state under current spending, taxes, exports, subsidies, debt, and exchange-rate conditions. A country with a $120 fiscal breakeven can still make money producing at $60. It just cannot fund the political economy it has built. Production cost determines who can keep pumping. Fiscal and political resilience determines who can keep exporting reliably.

That is why cheap barrels do not guarantee stability. Iraq has cheap barrels, but the Iraqi state depends on oil revenue to fund public payrolls, imports, subsidies, reconstruction, patronage, and federal-regional bargains. Iran has cheap geology, but sanctions, war exposure, regional commitments, and domestic pressure affect what the state can do with those barrels. Russia is a major producer with significant production capacity, but war spending, sanctions, discounting, shipping constraints, and technology restrictions change the netback and the political meaning of oil revenue. Libya has good oil, but rival authorities, militias, and export blockades turn production into a political weapon. Nigeria’s problem is not just geology. It is theft, sabotage, offshore cost, foreign-exchange stress, community conflict, and underinvestment. Venezuela has huge resources, but heavy oil, sanctions, degraded infrastructure, lost technical capacity, and governance failure make those resources far less useful than they look on a reserves table.

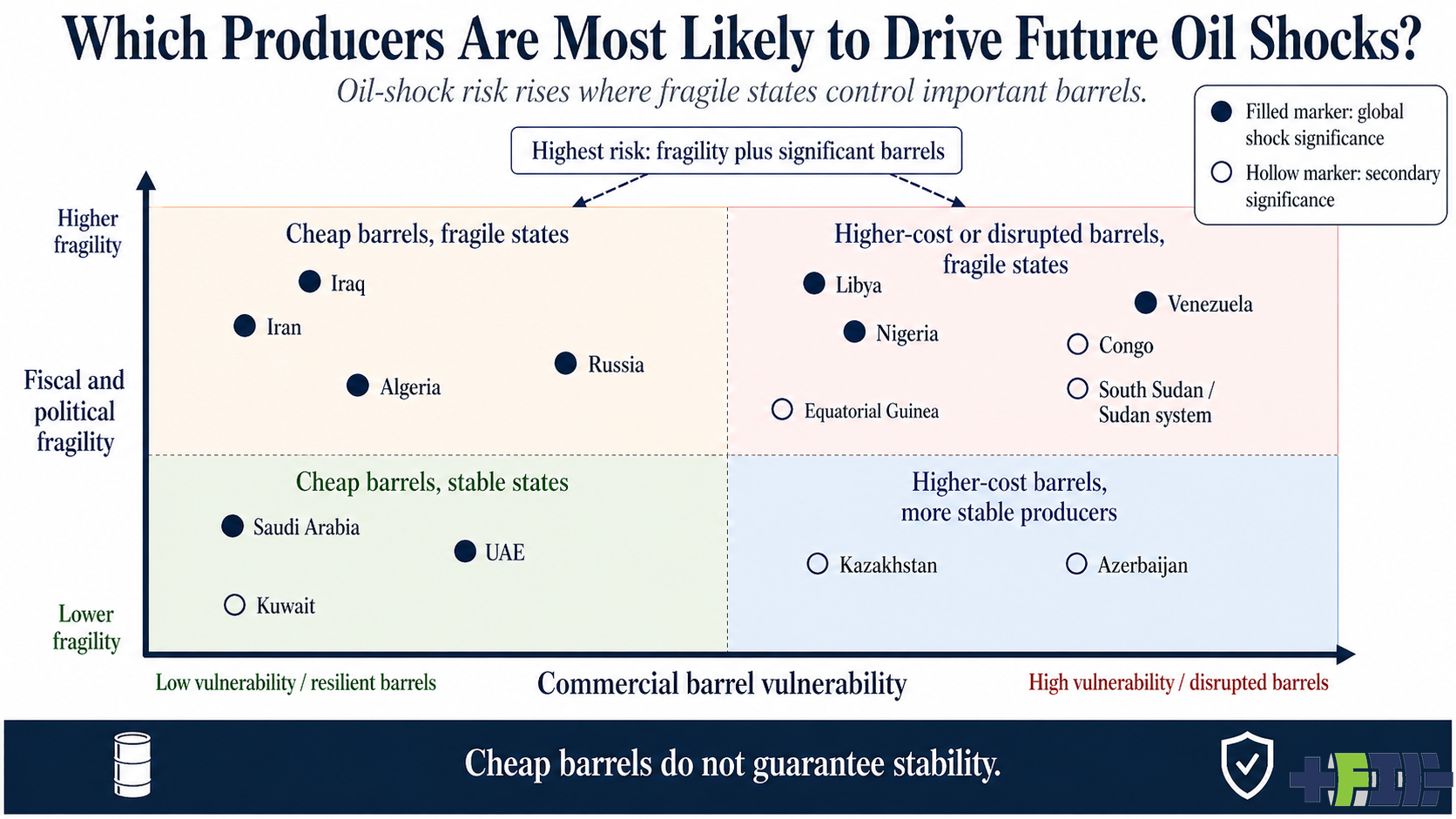

A useful risk matrix has commercial barrel vulnerability on one axis and fiscal and political fragility on the other. In the lower-left quadrant are cheap barrels in relatively stable states, including Saudi Arabia, the UAE, and Kuwait. These producers are not immune to low prices, but they have low-cost production, financial buffers, state capacity, and the ability to survive price cycles. In the upper-left quadrant are cheap barrels in fragile or geopolitically exposed states, including Iraq, Iran, Russia, and Algeria. Their barrels may be resilient, but the states and sanctions environments around them are not. In the upper-right quadrant are higher-cost or disrupted barrels in fragile states, including Libya, Nigeria, Venezuela, Congo, Equatorial Guinea, and the South Sudan and Sudan system. That is where production decline, export interruption, infrastructure problems, and state weakness can interact. In the lower-right quadrant are higher-cost barrels in more stable producers, such as Kazakhstan and Azerbaijan, although stability is relative in both cases.

The marker distinction in the matrix matters. A filled marker should mean global shock significance, not danger. Saudi Arabia and the UAE are globally significant because their production and spare capacity matter, even if they sit in the stable quadrant. Iraq, Iran, Russia, Libya, Nigeria, and Venezuela are globally significant because their instability or disruption can move markets. Hollow markers are secondary global significance. They can matter regionally or in specific product markets, but they are less likely to drive a global oil shock alone.

This framing avoids a common mistake. It does not say that the highest-cost barrels disappear first and everyone else is fine. It says that the oil system becomes unstable where commercial vulnerability, state fragility, and global significance overlap. Sometimes that is an expensive or disrupted barrel. Sometimes it is a cheap barrel controlled by a fragile state. The barrel cost is only one part of the risk.

OPEC+ faces a set of bad choices in this environment. The first option is defensive cuts. Saudi Arabia and the remaining core producers can cut supply to support prices. That can work in the short term, but it requires the strongest members to sacrifice volume while others may cheat, exit, or produce more outside the system. If demand is declining by 1 million to 2 million barrels per day per year, the group has to remove barrels every year just to keep the market balanced. Defensive cuts also create a demand problem. If OPEC+ supports $90 or $100 oil, it makes EVs, electric trucks, heat pumps, rail, remote work, and efficiency more attractive.

The second option is quota cheating. This is likely in a declining market. Members may sign on to cuts, then quietly exceed quotas, underreport, delay compensation cuts, push for higher baselines, or use opaque export channels. Cheating has always existed, but the incentive grows when producers believe future demand is at risk. The unsold barrel no longer looks like a store of future value. It looks like an opportunity cost.

The third option is a smaller disciplined core. OPEC+ may survive formally while the real coordinating group shrinks. Saudi Arabia, Kuwait, and a few aligned producers may coordinate more tightly, while the broader OPEC+ framework becomes a forum with less binding power. Institutions can outlive their market power. OPEC+ could still meet, issue communiques, and announce targets while traders place less weight on compliance.

The fourth option is a market-share war. Saudi Arabia could decide that cutting while others cheat is a poor bargain. In that case, it could defend market share rather than price, forcing prices lower and pressuring higher-cost producers, debt-heavy producers, and fragile states. This would echo 1986 and 2014, but with a different strategic backdrop. In previous episodes, Saudi Arabia was mostly fighting other oil producers. In the next episode, it would also be fighting electrification. Low oil prices can slow some marginal electrification, but they cannot easily reverse electric vehicle cost declines, China’s industrial strategy, depot charging economics, or the institutional desire to avoid oil shocks.

The fifth option is a downstream and diversification pivot. Producer states can invest in refining, petrochemicals, plastics, LNG, hydrogen, ammonia, metals, logistics, tourism, data centers, and sovereign wealth portfolios. Some of this makes sense as national strategy, and the UAE and Saudi Arabia have been doing versions of it for years. But it is not a clean OPEC+ solution. If every producer treats petrochemicals as the refuge of oil demand, petrochemical margins can be compressed. If every producer moves downstream, they compete with one another in another market.

The sixth option is explicit demand defense through lower prices. OPEC+ could decide that defending high prices is self-defeating and aim for a lower price band that keeps oil competitive. This is rational in theory, but hard in practice because producer states need revenue. Many have built budgets, subsidy systems, public payrolls, development plans, and political bargains around oil income. A lower-price strategy may protect long-term demand but damage short-term stability.

The interesting question is not whether OPEC+ survives as a name. It may. The more important question is whether it can still act as a reliable throttle on global supply. Under declining demand, that becomes less likely. OPEC+ can cut to defend price, but cuts accelerate substitution. It can avoid cuts, but lower prices stress producer states. It can tolerate cheating, but markets lose confidence. It can punish cheating, but price wars create fiscal damage. None of these paths restore the old growth-market bargain.

The likely price pattern is not a smooth glide path from $100 to $80 to $60 to $40. It is more likely a jagged path. A shock pushes prices to $120. Demand destruction and restored supply push them to $70. Quota erosion and weak demand push them to $50. Underinvestment or a producer disruption pushes them back to $90. Another demand leg pushes them to $45. A fragile-state conflict or chokepoint crisis pushes them back to $100. The direction of travel can be down while the lived experience is volatile.

Since 1973, major oil shocks have arrived roughly every four years, depending on how the boundary is drawn. That is about 13 major shocks over 53 years. In other words, the oil system has already been shock-prone in its growth era. The concern is that the decline era increases the cadence. If weaker demand undermines OPEC+ discipline, lower prices stress fragile petro-states, cautious investors reduce long-cycle supply, and chokepoints remain exposed, the historical average of one major shock every four years could tighten toward one every two or three years. The average price trend may be down, but the system becomes more brittle, so the shocks arrive more often.

Every spike changes behavior. A household may not replace a car during the first gasoline spike, but a fleet manager making a five-year procurement decision will remember it. A port authority considering equipment replacement will price fuel risk. A logistics company with predictable routes will reassess diesel exposure. A country importing most of its oil will see the balance-of-payments risk. A government dealing with inflation will see oil dependence as a political liability.

Electrification is no longer just a climate strategy. It is a volatility hedge, a national-security strategy, a balance-of-payments strategy, an industrial strategy, and a procurement-risk strategy. For importing countries, this is the key point. Declining oil demand does not mean oil is safe to rely on during the transition. It may mean the opposite. While oil remains large, the system can still shock economies. As the system shrinks, the stabilizers may weaken before dependence is gone.

For fleets, the math is not just fuel cost per kilometer. It is cost plus risk. Diesel at $1.40 per liter today and $2.20 during a crisis is not the same planning problem as electricity bought under a contract, partly supplied from on-site solar, buffered by batteries, and charged overnight. A battery-electric truck may cost more upfront, but if use rates are high and fuel volatility is material, the risk-adjusted economics improve. China’s heavy truck market is making this point faster than many analysts expected.

For cities, electric buses, electric garbage trucks, electric maintenance fleets, and electric ferries reduce exposure to diesel price shocks. For ports, electrified cranes, trucks, yard tractors, and shore power reduce exposure to bunker and diesel markets. For rail, electrification and battery-electric segments reduce fuel risk. For buildings, heat pumps reduce exposure to gas and oil heating volatility. For industry, electrified heat where technically practical reduces exposure to fossil fuel price cycles. None of this is instantaneous, but the direction is clear.

For oil exporters, the picture is uneven. The best positioned are those with low-cost barrels, large financial buffers, small populations relative to revenue, stronger institutions, and credible diversification strategies. The UAE, Saudi Arabia, and Kuwait are in that category, although even they face hard choices if oil revenue falls faster than expected. The UAE’s position is strengthened by diversified logistics, aviation, finance, real estate, and sovereign wealth, as well as by production flexibility after leaving OPEC. Saudi Arabia has scale, low costs, and reserves, but also large spending commitments. Kuwait has wealth and low-cost oil, but political constraints.

The most politically exposed exporters are different. Iraq, Libya, Nigeria, Iran, Venezuela, and the Sudan and South Sudan system face combinations of oil dependence, weak institutions, conflict exposure, sanctions, militias, public payroll pressure, infrastructure damage, and regional disputes. Lower oil prices do not mean these countries stop producing because the barrel is unprofitable. They mean the state has less room to maintain the bargain around the barrel.

Russia sits in its own category. It is a major producer and a global shock node. Lower prices pressure war finance, the ruble, regional spending, military procurement, and state capacity. But Russia also has coercive tools and a large state apparatus. The risk is not simple collapse. It is fiscal stress combined with war, sanctions, repression, and external-risk behavior. That can still produce oil-market volatility.

Algeria is a quieter risk. It is not Libya, Iraq, or Iran. But high fiscal dependence, subsidy expectations, youth pressure, and a state-centered political economy make long periods of low oil and gas prices uncomfortable. Kazakhstan is also not a simple case. It is more stable than many fragile producers, but has social unrest history, a hydrocarbon-heavy fiscal base, and export-route exposure. These are not the first names in a global shock story, but they belong on the watchlist.

For importing countries, the implication is direct. Do not confuse lower average oil demand with lower oil risk. Oil can be less important over time and still create major shocks along the way. The correct response is to accelerate the parts of electrification that reduce exposure fastest: passenger EVs, buses, delivery fleets, depot-charged trucks, rail, ports, ferries, heat pumps, and industrial heat where electricity is already practical. Domestic renewables, batteries, flexible demand, and grid upgrades are not just climate infrastructure. They are fuel-risk reduction infrastructure.

The same logic applies to aviation, but with a different toolset. Long-haul aviation is hard to electrify. But demand can be managed, business travel can be reduced, short-haul routes can shift to rail where infrastructure exists, and airlines can become more exposed to fuel efficiency and alternative fuels. EU aviation policy is already pushing in this direction through emissions pricing and SAF requirements. SAF does not make aviation cheap. In many cases it makes the cost of flying more visible. That may depress demand at the margin, especially for discretionary and business travel.

There are clear indicators to watch. China’s gasoline and diesel demand are the most important early signals. Battery-electric heavy truck sales in China matter because diesel is a core oil product. Global EV fleet penetration matters more than annual EV sales, because oil demand is displaced by kilometers driven, not showroom headlines. Aviation fuel demand and business travel recovery matter because aviation is often used as the growth offset in oil-demand forecasts. OPEC+ quota compliance matters because it reveals whether members still believe in the bargain. UAE production after leaving OPEC matters because it tests whether flexibility beats discipline. Saudi willingness to cut matters because Saudi Arabia remains the fulcrum of supply management.

Other watchpoints are more political. Iraq’s public-sector wage burden, Libya’s export interruptions, Nigeria’s oil theft and foreign-exchange stress, Russian oil discounts and shipping constraints, Iranian sanctions and regional conflict, and Algeria’s subsidy pressure all tell us whether fiscal stress is moving from spreadsheets into political reality. Upstream capital spending matters because too little investment can create future supply tightness even in a declining-demand world. Diesel and jet fuel markets matter because product bottlenecks can create price shocks even when crude looks adequate. Tanker rates, insurance costs, and chokepoint risks matter because oil is still a physical commodity moved through narrow corridors.

The important thing to understand is that lower oil demand does not mean lower oil risk in a straight line. It means the risks change shape. Oil’s long-term strategic importance falls. Its average price power weakens. But its short-term volatility is likely to rise because the system around it becomes more brittle. The petroleum age is unlikely to end with one dramatic crash. It is more likely to enter a volatile decline, with each shock strengthening the case for electrification, and each wave of electrification weakening the future demand that once held the oil system together. The countries, cities, companies, and households that understand this will not wait for the last oil shock to pass. They will build around electricity because electricity is not just cleaner. It is more controllable.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy